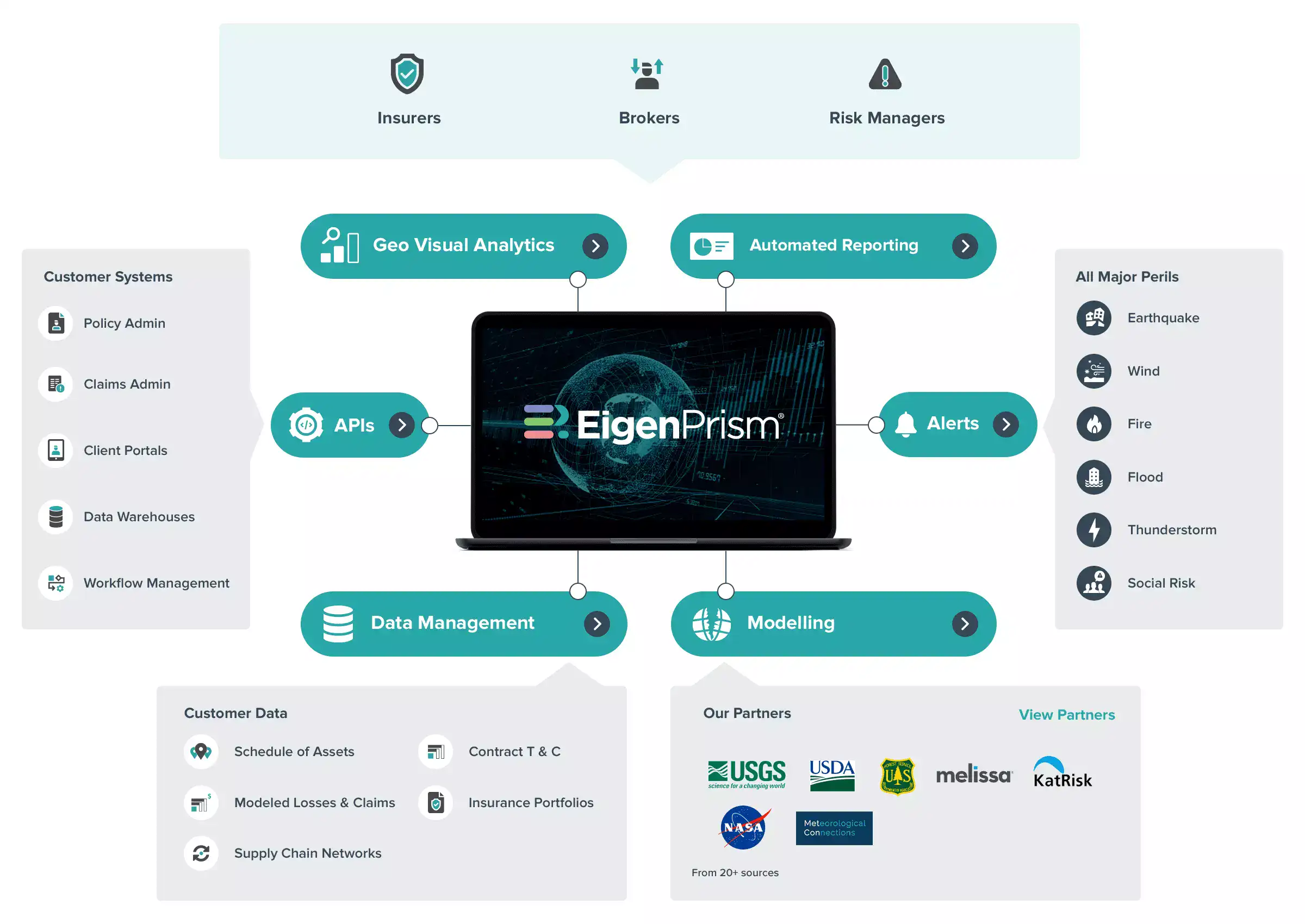

Improving Data Quality for a Better Insurance Renewal

Prior to its 2016 property insurance renewal, the Risk Management Department of the Miami Dade County School District, like many other organizations, viewed the insurance renewal process as a somewhat perfunctory annual exercise.

But this year was different: Michael Fox, Risk & Benefits Officer, reviewed the modeled loss results and intuitively, knew the models were off. He was not sure what was causing the discrepancy, but he knew his risk well enough to ask his broker to question the model results. And with 10,000 locations to manage, data quality was a logical starting point for their review:

- Original modeled loss results showed an Average Annual Loss (AAL) of $826M

- AAL is used to determine adequacy of insurance limits, and is therefore influenced by the quality of location level data

- Values collection is a highly manual process, prone to quantitative and qualitative errors

Using EigenPrism, the broker uploaded and ran the Miami-Dade County Schools schedule of values. The data visualization and mapping tools immediately identified that 20% of the locations were geo-coded incorrectly. Some of the locations were in Biscayne Bay, while another location was actually in China. As the probabilistic model loss results were based on this incorrect data, the risk manager’s intuition was correct: location data and COPE characteristics were not being accurately reflected in the model assumptions, generating misleading loss results, which would negatively impact their insurance renewal.

When resubmitted for modeling, with the corrected location data, the AAL was reduced by 30% – approximately $250M.

Despite the improvement in modeled loss results, the risk manager knew the AAL was still too high, but had no empirical data to challenge this market required probabilistic loss result. Rather than deciding solely on a theoretical set of statistical calculations, could the Risk Management department complement the model by computing the ground up losses for all historical south Florida hurricanes, and run a worst-case scenario?

This type of deterministic analysis would provide the data needed to stress test his program limits against the computed AAL.

Using EigenPrism, the school system modeled 1992 Hurricane Andrew as a worst-case scenario and found that the ground up loss was $622 million, compared with the $826 million traditional models had calculated.

Michael Fox, Miami Dade County Schools

This second perspective provided a reality-check for the probabilistic loss results, giving them the confidence needed to optimize their insurance renewal.

EigenPrism emboldens risk managers and brokers with the power to analyze their own exposure data – the basis for modeling and pricing. The ability to simulate different permutations of events with scientifically developed models helps level the playing field in insurance renewals. It gives risk managers such as Miami Dade County Schools the confidence to select the appropriate limits, retentions and conditions to their insurance programs.

When we utilize EigenPrism’s capabilities…it’s a valuable tool that helps shape our view of risk.

Michael Fox, Miami Dade County Schools

{kind=link}