New Technology Helps Brokers, Risk Managers Manage Complex Property Risks

Today, creating effective global property insurance programs involves both the efficient deployment of underwriting capacity and the accurate modeling of significant risks, including those from catastrophic events. Accordingly, risk managers typically consider the potential impact of 100-, 200-, and even 500-year catastrophic events on their property portfolios to determine their coverage needs.

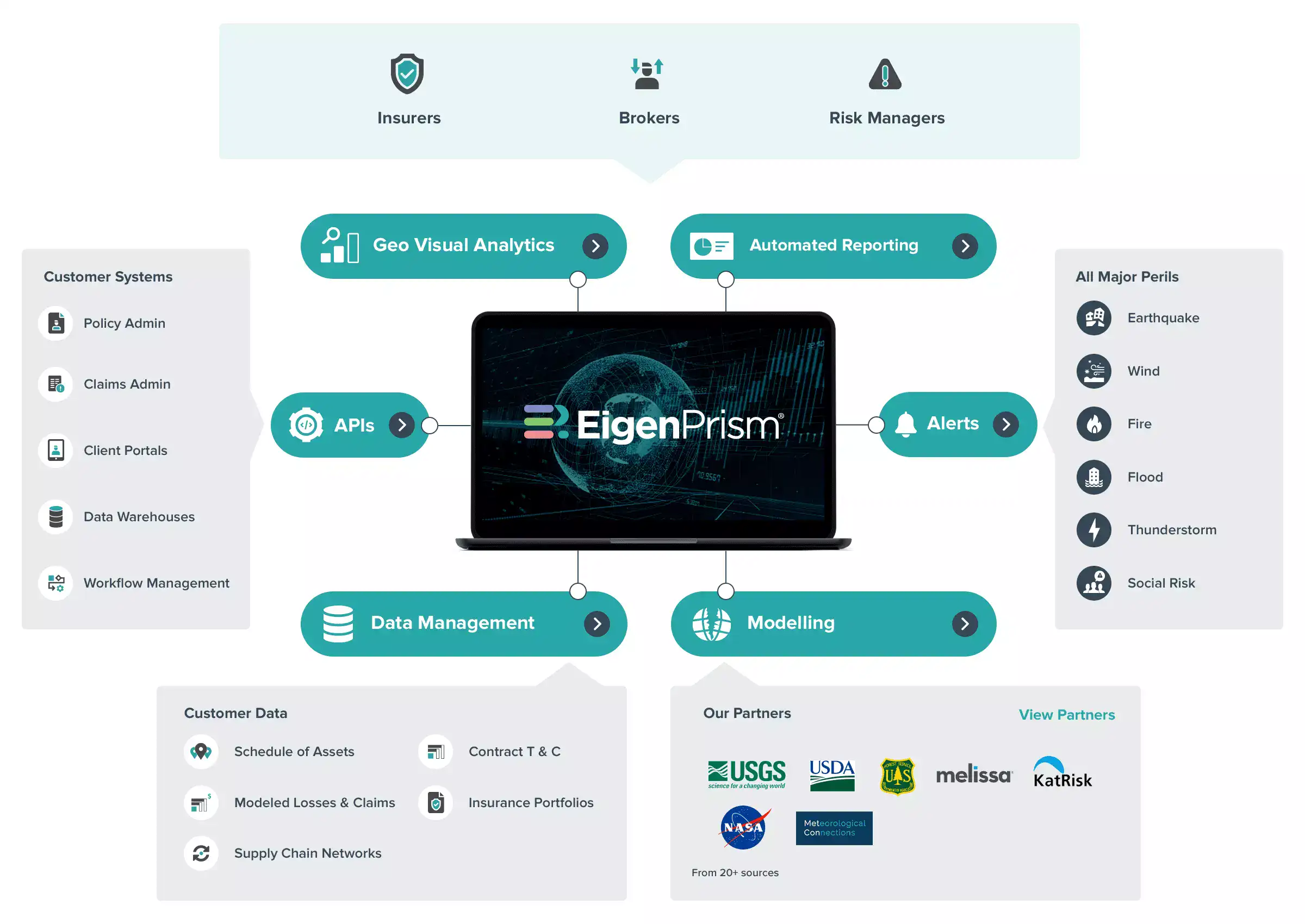

While the analytics can be complex, technology can reduce the time required to complete them; improve placement results; simplify program recommendations, and enhance the overall client experience on insurance renewals or new placements.

By leveraging big data platforms and modeling, brokers and risk managers can strengthen each element of their insurance placement process, including:

- Stress testing. By running different loss scenarios based on past events, such as hurricanes and earthquakes, risk managers can better understand the potential impact at specific locations and assess the adequacy of their insurance. Open analytics and modeling platforms enable brokers and risk managers to run multiple permutations of loss events so they can make informed assessments of their coverage needs.

Insurance programs involving multiple policies are fungible, so positions often can be moved, changed or replaced, enhancing the insured’s ability to obtain desired protection at the best available terms. The renewal process includes a standard submission packet with updated statement of values spreadsheets, coverage specifications, engineering reports, loss reports, etc. Today’s technology enables this data to be presented to underwriters in dynamic ways that can differentiate the account and improve the outcome.

- Given the widened availability of open risk analytics and modeling platforms brokers and risk managers now have access to the same technology tools used by underwriters to evaluate and price risks. Thus, insureds and their brokers can “pre-underwrite” the risk and negotiate more effectively with insurers. This also helps insureds obtain appropriate coverage limits, reducing the likelihood of a claim recovery shortfall in severe loss events.

- A key challenge in predicting how a program structure will perform involves the time required to run multiple loss scenarios. Historically, this required taking a policy’s terms and conditions, pasting them onto a spreadsheet, and running one simulation at a time. Digitizing your program structure so the policy language is embedded in your analytics platform can reduce errors and provides decision-makers with greater insights regarding how much risk to retain or transfer.

- By increasing the use of analytics and modeling, risk managers and their brokers will be better equipped to evaluate their data-driven options, including the adequacy of coverage limits, risk retention versus transfer, and create optimal program structures. Further, new technology facilitates real-time and continuous evaluation. This helps ensure the insurance program and risk management operate effectively through the duration of the policy term.

Today, as always, relationships, market knowledge, technical proficiency and the financial strength of participating insurers are keys to creating a resilient insurance program that can withstand both frequent and severe losses. Technology and analytics can help reduce the time and expenses associated with the insurance placement process and result in insurance programs that deliver protection when and where it’s most needed.

NOTE: This blog entry was adapted from an article by the same author that originally appeared in PropertyCasualty360 on Nov. 13, 2015. To read the full article on PropertyCasualty360, click here.

{kind=link}