Quantitative Corporate Risk Management – Ready for Take Off

With the commercialization of advanced analytics originally developed for institutional users, constituents across the insurance supply chain are being empowered collectively with technology that will disrupt how risk is selected, transferred and managed.

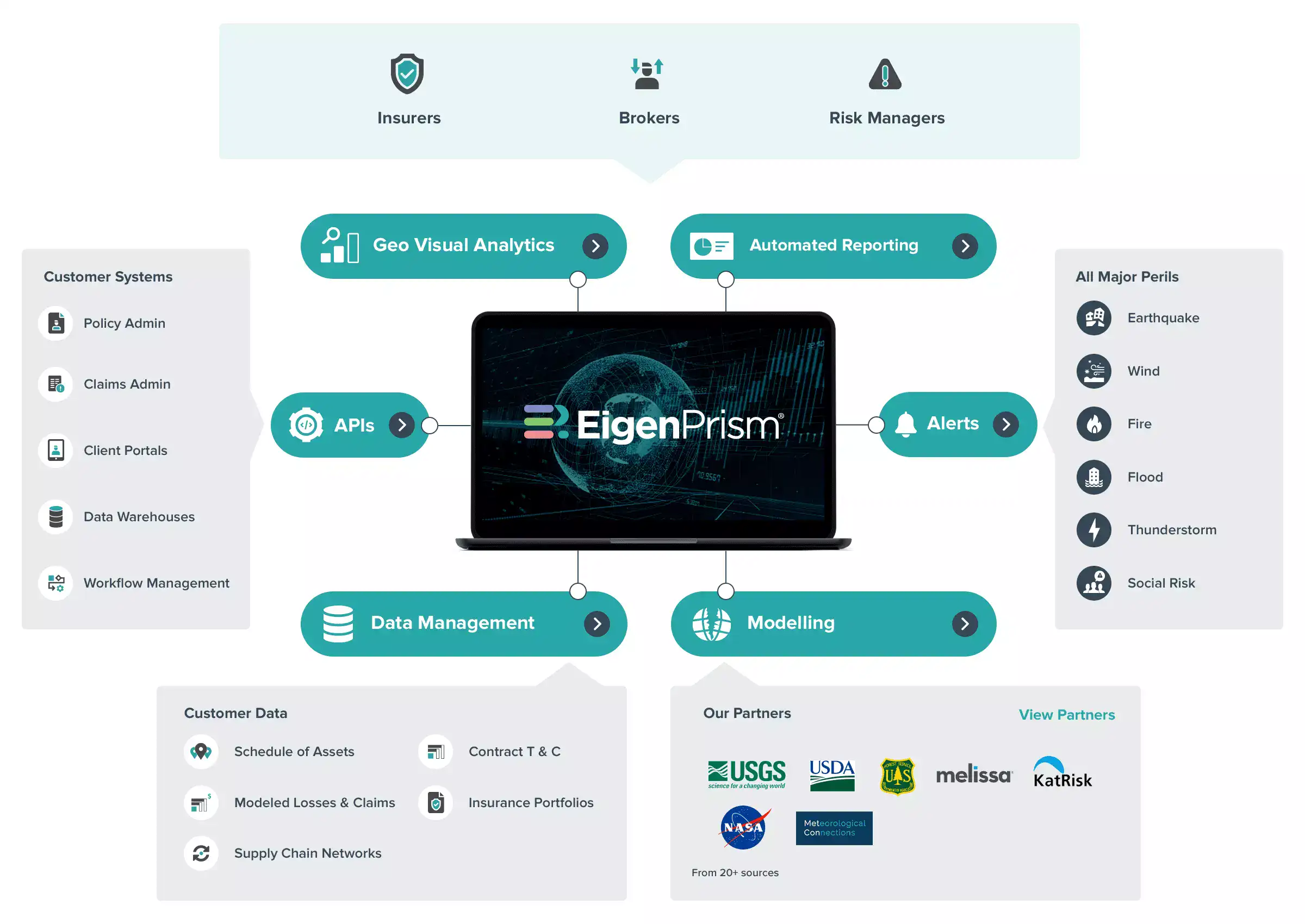

The risk and insurance industry is incipiently moving to a data driven and analytics-based business similar to other financial institutions. Today’s Big Data and computational power is enabling risk managers to make faster and better decisions through speed-of- thought analytics.

Historically, risk and insurance management have been static functions with business processes designed to capture and manage qualitative exposure data such as COPE*, Replacement Cost Values, PML/ MFL/ EML’s**, Engineering, Claims, Incidents, etc. Many processes such as renewal management, program administration, and event response were managed either as scheduled or ad hoc activities in collaboration with intermediaries and carriers. Once these activities were performed, the data captured was often not re-used until the following year, and sometimes even “re-created” every year.

A new generation of quantitative risk management built on speed of thought analytics will process inputs such as exposures (what risk do we have) into strategic outputs (how much risk should we retain or transfer). By empowering corporate risk managers with such analytics technology, companies will enhance their attractiveness in the insurance marketplace statically at program renewal and continuously throughout the life cycle with a dynamic real time view into their risk portfolio. Risk Managers will not only achieve efficiency in the administration of programs, but will also increase the risk intelligence of their organization. They will be capable of pro-actively managing their own risk with the same analytical methodologies as financial institutions. For example, they will be able to

- Conduct loss simulations and exposure accumulation analysis powered by a library of historical footprints (events) and advanced analytic algorithms developed by the larger modelling community made up of PhD’s, mathematicians and actuaries;

- “Model a policy” and calculate estimated payments by flowing losses through the terms and conditions at the location or portfolio level;

- Proactively respond to real time events through alerts and loss estimates including impact of complex supply chains;

- Calculate program erosion in real time;

- Estimate technical pricing to reduce pricing uncertainty and approach renewal negotiations with more confidence.

Quantitative risk managers operating in an open and intelligent system are expected to drive value to the insurance industry by originating higher quality exposure data into the eco-system, increasing service efficiency for intermediaries and underwriting efficiency for (re)insurers. This may also serve to smoothen the variability inherent in insurance market cycles. – all for the ‘common good’.

Launching commercial GPS satellites on rockets required the application of advanced mathematics and science Today, GPS is used commercially by nearly a billion people with a diverse set of users such as aviation, public safety, disaster relief and recreation.

In the same way, the latest generation of high performance computing and Big Data technology will help empower a new generation of corporate risk managers to navigate the rapidly changing insurance landscape. They will own and control their risk life cycle as well as their data across the insurance supply chain. For corporate risk managers, owning your risk is a simple concept, not rocket science. And it’s taking off faster than you think.………

Eduardo Hernandez is a co-founder and Business Development leader for EigenRisk, a risk analytics company serving the (re)insurance, intermediary and risk management community. He has 20 years of risk and insurance management experience in underwriting, placement, product development and sales.

* COPE = Construction, Occupancy, Protection, Exposure, ** PML= Probable Maximum Loss, MFL = Maximum Foreseeable Loss, EML= Estimated Maximum Loss