Thinking outside the box for underwriting moratoriums

When a hurricane is imminent, insurers will generally not issue policies for locations in the storm’s path. These underwriting moratoriums are temporary stoppages based on a traditional “in the box” approach: as soon as the eye of the storm enters a pre-defined “box” with a certain strength, underwriting moratoriums are issued for that area. No policy coverage can be bound while the storm is “in the box”.

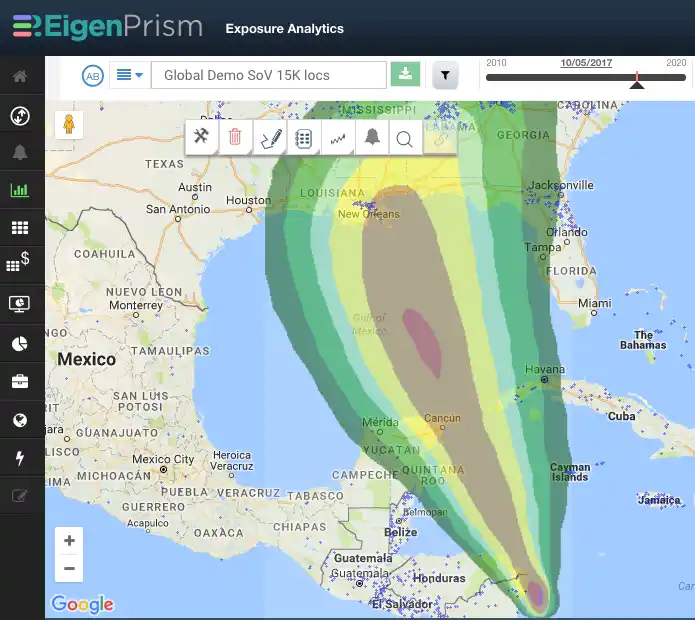

With advancements in hurricane forecasting, however, there are now much smarter methods to set moratoriums. For example, it is possible to obtain the probability of winds exceeding hurricane force at a single location up to 5 days in advance. These probabilities are the result of running hundreds of possible scenarios, and are already conservative, being intended for life safety. With this new approach, underwriters can assess the probability of an account being impacted by the impending hurricane well in advance and set or lift moratoriums on an account by account basis. Of course, there will still be judgment involved in determining the degree of conservatism used, but the final decision will leverage the best scientific models in real time, leading to fewer missed opportunities.

This was the case with Hurricane Matthew. Using the automated notifications from EigenAlert, underwriting managers customized their moratoriums based on forecast wind speed probability thresholds. The alerts were updated with every new forecast during the event, ensuring the underwriting team were always optimizing the area covered by the moratorium.

A simple way to use the latest science and technology for a competitive advantage!

{kind=link}