Global Risk – Juggling The Responsibility

Global risk management requires effective regulatory oversight. Regulation in Latin America leaves the management of environmental risks the responsibility of companies, so mitigating and insuring those risks is a choice businesses have to make.

While Central and North South America face the consequences of hurricanes and tropical storms, the South of the continent often endures severe droughts or destructive floods.

The World Economic Forum Identified Climate Change Mitigation As Global Risk

Climate change is expected to increase the frequency and severity of extreme weather events, causing increased damage to ecosystems, agriculture and human health. The consequences of climate change are visible throughout Central and South America. Early this year the Venezuelan government imposed energy rationing in Caracas, after a drought, caused by the El Niño phenomenon, brought 18 of the country’s hydroelectric dams to critically low water levels.

The drought is also affecting Central America, where the Panama Canal is to impose new depth restrictions on ships, due to falling water levels in lakes that form part of the waterway between the Atlantic and Pacific Oceans.

Last year Brazil also faced what was considered the worst drought in the country’s history, when the Cantareira interbasin transfer system, comprised of six dams, that provide water for almost 9 million people in the region of São Paulo, had water reserves drop to 5% of capacity.

These extreme events are rising the environmental awareness of companies operating in the region. New risk management tools and better insurance covers are now part of many companies’ strategy to mitigate environmental risks. Mike Andler, head of Lockton’s U.S. Property Practice, says that businesses are now more aware of the consequences of climate change to their operations.

“Over the past few years our clients have been increasingly concerned about climate change risk, from how a changing climate may affect physical assets and natural resources critical to operations, to regulatory costs as climate policies are enacted, to liability exposures stemming from damages associated with historical greenhouse gas emissions,” Andler says.

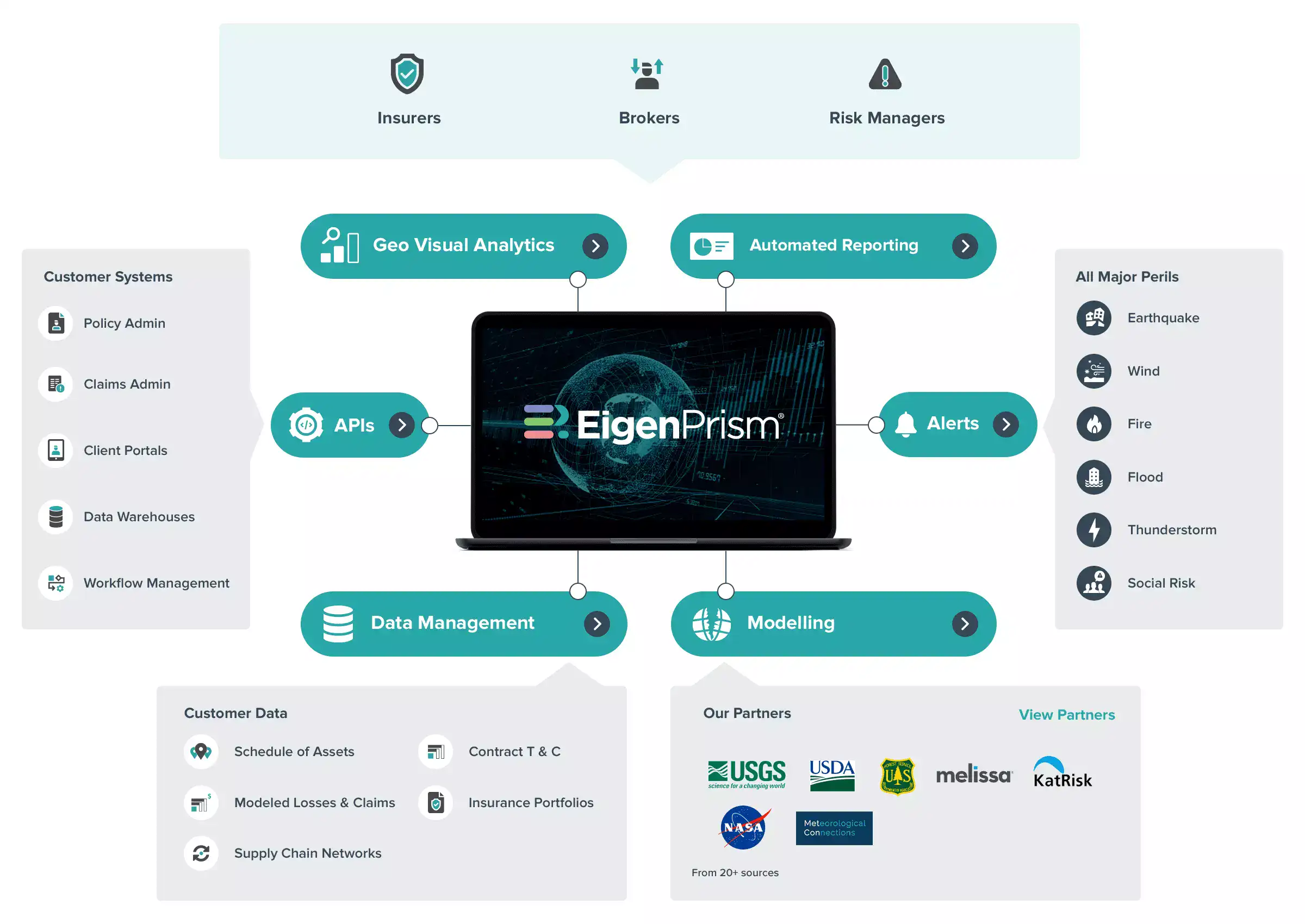

In his view, “given the recent frequency and scale of catastrophic events in Latin America, such as earthquakes and flooding, it’s clear that those charged with managing or mitigating risks need the appropriate tools and analytics to be more self-sufficient in data discovery, scenario planning and modelling, leading to faster and better informed business decisions”.

Lockton has recently launched a new platform for catastrophe exposure analytics and modelling, EigenPrism, available across Latin America.

“In addition, the protection gaps that were discovered after large catastrophic events, such as supply chain and interdependency losses, spurred the need to increase Contingent Business Insurance that traditionally had low sub-limits,” Andler adds.

Poor Regulation

Regulation plays a key part in the environmental insurance market in Latin America, as until now, businesses in many countries have benefitted from outdated reserving requirements for environmental risks.

Nonetheless, according to Andler, there is a growing trend by governments to enact regulations that will require more underwriting rigor to local insurance companies, such as detailed COPE and Geo coded locations.

For instance, Colombia has recently passed regulation Decreto 4865 and 2555, that will change how a company’s earthquake risk is underwritten and priced.

Still, “liability insurance is not very popular in Colombia and penetration of this business line remains very low,” says Camila Martínez, public liability and compliance chamber director for Fasecolda, the Colombian insurers’ association.

Martínez considers that in consequence, unless coverage became mandatory, it seems unlikely that people will require it.

In 1999 the 491 law was promulgated, and this was the first attempt to implement a general mandatory environmental liability insurance in the country. But Martínez explains that the lack of clarity about the extent of the coverage made its implementation nonviable.

Currently, only the coverage for sudden and accidental contamination is mandatory (Decree 3112, 1997 and 4299, 2005). Some activities, like transportation, handling and storage of hazardous substances and dangerous goods, do require an environmental liability coverage by law.

The fact that Colombia does not have a mandatory general insurance law, that covers losses raised from environmental accidents for all the activities that represent an ecological risk, like in many other countries in Latin America, means that environmental responsibility lies with each company.

“Apart from the mandatory insurance coverages, some casualty policies are including a voluntary coverage for contamination, which is explained by the identification of the risk from some insured and the worry of having to face it on their own,” Martínez says.

She says that generally, for both mandatory and voluntary environmental liability insurances, the coverage extension is for sudden and accidental pollution that causes bodily injury, property damages, and clean up and restoration related to the loss.

Dan Negron, senior underwriter for TT Club Americas, adds that in the marine industry most general liability policies in the insurance market today contain a feature that provides cover for sudden and accidental pollution.

“However, as the name implies, this does not insure an operator for long term pollution risks, such as where long term seepage is discovered years after a pollution event has taken place. For risks of this nature, an operator needs to procure a specialist policy that can be procured in the global insurance market,” he explains.

The lack of appropriate environmental protection regulation in Latin America leaves each business to decide which risk management strategies and insurance covers to adopt for its operations. This is a big responsibility that companies can not overlook.

{kind=link}